Trends In Exit Activity For The Singapore Startup Ecosystem

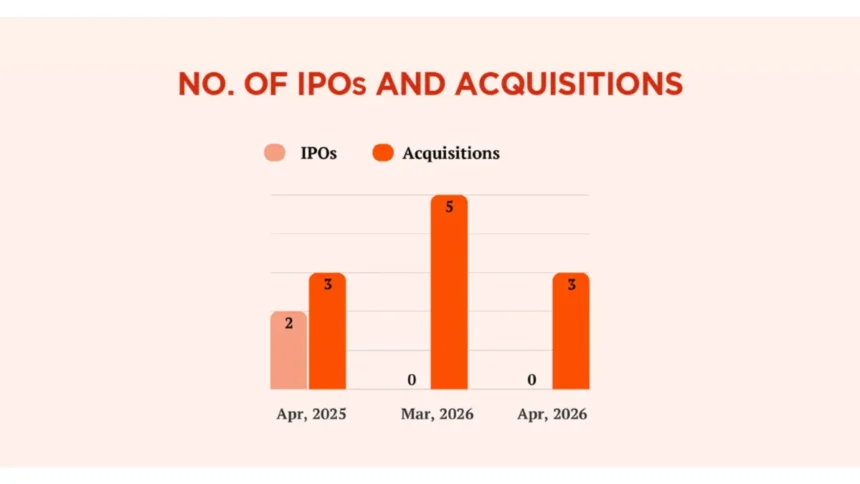

The landscape for regional innovation remains focused on consolidation as every Singapore startup navigates a market defined by strategic acquisitions rather than public listings. According to the latest data compiled by market intelligence platform Tracxn, the month of April 2026 saw a notable shift in how companies achieve liquidity.

While the total number of acquisitions reached three, this represented a slight cooling from the five deals recorded in the preceding month of March. More significantly, the initial public offering market remained entirely dormant for the second consecutive month, a sharp contrast to the same period in 2025 when the exchange welcomed two new public listings alongside three private sales.

This absence of IPO activity suggests that founders and their venture capital backers are currently prioritizing private exits or waiting for more favorable conditions to tap into the public equity markets. Interestingly, the month still managed to produce one new unicorn, highlighting that high valuation potential remains present even when the exit path is narrowed toward corporate buyouts.

These acquisitions covered a broad spectrum of maturity levels, spanning from early stage innovators to growth stage organizations, though specific transaction values for the buyouts were largely kept confidential within the current dataset. This trend reflects a broader maturing of the digital infrastructure where established players are looking to absorb niche technologies to enhance their own market positions and operational efficiencies.

Capital Allocation And Funding Rounds In The Early Stage Market

Despite the quiet nature of the public markets, the venture capital environment continues to deploy funds across various maturity cycles to ensure the next startup can scale effectively. Seed stage funding emerged as a significant highlight in April, reaching a total of 28.2 million dollars and demonstrating a robust appetite for fresh ideas and foundational technology.

Early stage rounds contributed an additional 3.7 million dollars to the ecosystem, while late stage funding totaled approximately 7.8 million dollars during the same period. This distribution of capital indicates that investors are currently more comfortable placing smaller, diversified bets on nascent companies rather than committing to massive late stage checks during a period of exit uncertainty.

Over the past twelve months, the exit landscape has been characterized by sporadic IPO occurrences, leaving acquisitions to form the primary backbone of reported exits for most technology firms. The largest individual deal during the month was a 15 million dollar round secured by Simple Chain, followed closely by a 7.8 million dollar investment into Biobot Surgical by ZIG Ventures.

Other notable capital injections included Accel backing Atlas with 6 million dollars and Betatron Venture Group providing 3.7 million dollars to CubeAsia. These figures suggest that while the blockbuster exits are on pause, the fundamental plumbing of the ecosystem remains functional, with diverse sectors like surgical robotics and retail analytics continuing to attract institutional interest.

Strategic Outlook For Regional Innovation And Market Liquidity

The current state of the market suggests that any emerging startup must now focus on achieving a path to profitability or a strategic sale rather than banking on a quick public debut. With no IPOs recorded in the recent data, the burden of providing liquidity to investors falls squarely on the shoulders of the mergers and acquisitions market.

This shift is partially driven by global financing conditions that have made the cost of capital more expensive, forcing both buyers and sellers to be more disciplined in their valuation expectations. The fact that KieDex secured 3.5 million dollars and Golden Gate Ventures invested 1.7 million dollars in Ortcloud shows that specialized firms are still finding value in smaller, more agile teams.

As we look toward the second half of 2026, the success of the ecosystem will likely depend on whether the backlog of mature companies can eventually find a window to list on the stock exchange. Until that happens, the dominance of corporate acquisitions will continue to define the lifecycle of technology investments in the region.

Maintaining a strong balance sheet and demonstrating clear commercial utility has become more important than ever for founders seeking to attract the next round of backing. By focusing on essential human needs and infrastructure based solutions, these companies can better insulate themselves from the volatility of the capital markets and remain attractive targets for both domestic and international acquirers.

Startup Exit Velocity And Ecosystem Maturity

The absence of public listing activity in the April 2026 data reflects a broader global retrenchment in the technology sector where valuation discovery remains a primary challenge. The reliance on acquisitions as the sole exit mechanism for a Singapore startup indicates a narrowing of the liquidity funnel, which could potentially impact the recycling of capital back into the early stage ecosystem if prolonged.

When venture capital funds cannot realize gains through the public markets, the speed at which they can return capital to limited partners slows down, creating a bottleneck that affects the next generation of founders. However, the consistent flow of seed stage funding at 28.2 million dollars provides a necessary counter-narrative, suggesting that long term conviction in the regional digital economy remains intact.

The regional market impact of this trend is significant, as it solidifies the city state’s role as a primary incubator for high quality assets that are eventually absorbed by larger multinational conglomerates. This consolidation phase is essential for the long term health of the industry, as it allows for the integration of innovative digital tools into more established business frameworks without the immediate pressure of public quarterly reporting.

We project that as global interest rates stabilize in late 2026, the bid-ask spread between startup founders and public market investors will begin to close, potentially reopening the IPO window for the most resilient players. For now, the focus on practical, infrastructure focused fields and strategic buyouts provides a defensive layer of stability for the finance and investment community.

As the sector continues to mature, we expect to see more sophisticated deal structures that prioritize earned milestones over speculative growth, ensuring that the next wave of exits is built on a foundation of genuine fiscal sustainability. This ensures that the Southeast Asian innovation corridor remains a premier destination for institutional capital, even as the global exit landscape undergoes a fundamental recalibration.