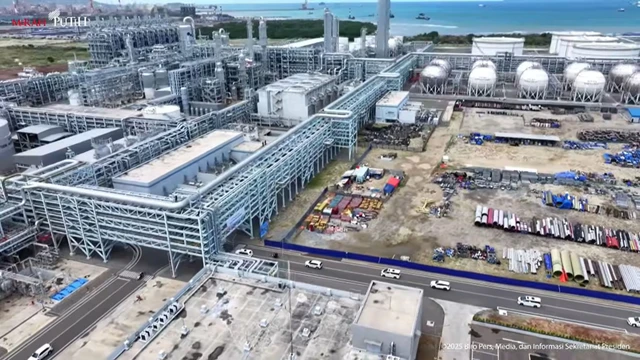

Short Term Earnings Rebound For Lotte Chemical Titan

The Malaysian petrochemical sector is witnessing a localized shift in sentiment as market analysts upgrade their outlook for Lotte Chemical Titan Holding Bhd. According to a recent note from Maybank Investment Bank, the company has been moved to a hold rating, which notably stands as the only non-sell call currently issued for the stock. This transition in perspective is primarily driven by an anticipated short-term earnings boost resulting from the consumption of lower-cost naphtha inventories.

In the first quarter ending March 31, 2026, the group is expected to narrow its recent losses significantly, with a potential return to profitability during the second quarter. The financial valuation of the firm saw an immediate reaction to this news, with the stock price climbing to 35 sen and valuing the group at approximately 797.15 million Ringgit. Investors are currently looking at a narrow window of trading opportunity, as the near-term rebound is fueled by a specific six-week lag between the procurement of raw materials and their actual consumption in production.

This timing allows the company to capture a stronger spread since the prices for petrochemical products have already adjusted upward following major supply disruptions in the Middle East. While the broader industrial environment remains challenging, the strategic use of existing stock provides a temporary cushion against the volatile global market. The ability of the management to navigate these complex procurement timelines will be the determining factor in whether the firm can successfully bridge the gap before higher-cost feedstocks begin to impact the operational bottom line.

Feedstock Constraints And Operational Risks In 2026

The immediate advantages enjoyed by the petrochemical giant are expected to be relatively short-lived as the ongoing conflict in the Middle East begins to choke global supply chains. Financial analysts have warned that a significant portion of the feedstock used by Lotte Chemical is sourced directly from that region, and current inventories may only be sufficient to support full-scale operations until the end of May. Beyond this point, the lack of available naphtha could force the company into a difficult position.

This could potentially lead to a forced production cut or even a total halt starting in June 2026. There is a growing concern that the group might have to declare force majeure if it cannot secure enough raw materials or if the feedstock spreads fall below the critical threshold of 300 US dollars. Such an unusual production environment would make continued operations economically unviable, as the breakeven point for high-density polyethylene is estimated to be between 550 and 600 US dollars.

Currently, the spread stands at a healthy 900 US dollars, but this margin is temporary and will likely fade once the higher-cost supply reaches the manufacturing stage. A prolonged disruption in the Strait of Hormuz could result in suboptimal operating rates and lower cracker utilization, which would fundamentally alter the group’s financial trajectory for the remainder of the fiscal year. The research house has already adjusted its net loss forecasts for the 2026 and 2027 periods, assuming that production halts will be necessary to cap the gross losses that occur during periods of extreme input price volatility.

Strategic Outlook And Regional Petrochemical Market Impact

From a professional analytical perspective, the situation facing Lotte Chemical reflects a broader trend of defensive positioning sector across the ASEAN region. We analyze that the decision to halt production across major operating plants is a sophisticated risk-mitigation strategy designed to stop the bleeding of capital during periods where every unit sold results in a gross loss. By assuming an average price of 1,400 US dollars per tonne for high-density polyethylene, the market is pricing in a scenario where supply scarcity dictates the valuation.

We project that if the regional energy crisis persists through the second half of 2026, the Malaysian petrochemical industry will undergo a significant structural shift toward more diversified sourcing strategies to reduce dependency on the Middle East. The synergy between financial resilience and operational agility is now the cornerstone of the group’s survival plan, as it attempts to weather the storm of cost-push inflation. The market consensus remains cautious, with three sell calls still weighing on the stock despite the lone hold rating.

This divergence in opinion highlights the high-stakes nature of trading during a geopolitical crisis, where timing is everything. Furthermore, the potential for a production stoppage from June to December of 2026 implies a significant gap in the regional supply of essential plastics, which could ripple through the manufacturing and packaging sectors in Southeast Asia. We anticipate that this supply vacuum will lead to higher downstream costs for consumer goods, reinforcing the inflationary pressures already present in the regional economy.

Regional Economic Vulnerability And Downstream Industrial Impacts

The potential operational halt of Lotte Chemical in Malaysia creates a systemic ripple effect across the ASEAN manufacturing core that extends far beyond simple equity valuation. From an expert B.I.F.E. perspective, we analyze that a production vacuum in Malaysia will likely force downstream manufacturers in Thailand, Vietnam, and Indonesia to source high-density polyethylene from more expensive American or European suppliers. This logistical shift in 2026 will inevitably inflate the cost of goods sold for regional packaging, automotive, and construction industries, potentially leading to a margin squeeze for smaller enterprises that lack the hedging capacity of larger conglomerates.

We project that the regional reliance on Middle Eastern naphtha has reached a critical inflection point, necessitating an urgent diversification toward bio-based feedstocks or increased domestic refining capacity. The current 900 US dollar spread is an oasis in a desert of supply chain instability, and we anticipate that regional governments will soon intervene with temporary tariff adjustments to protect local manufacturing jobs if production stoppages become widespread. The risk here is a localized industrial stagflation, where high material costs collide with cooling consumer demand as the broader economy absorbs the impact of 2026 energy prices.

Furthermore, the fiscal health of the Malaysian industrial sector is at risk of a credit rating recalibration if key petrochemical players are forced into prolonged force majeure scenarios. We observe that institutional capital is already beginning to pivot toward service-oriented sectors or energy-independent technology hubs to avoid the volatility of the materials market. The synergy between geopolitical stability and regional industrial output has been fundamentally compromised, and the ability of firms to bridge this supply gap will define the winners and losers of the ASEAN economic landscape for the next three to five years.